When calculating unit costs in mechanical manufacturing there are many factors to take into account. Apart from general costs, energy costs, wage costs, taxes and social contributions, the costs of the machine tool used in the manufacture is usually the most significant item.

It is worthwhile to look closer at the cost of the machine tool which is used to carry out a certain operation. This is particularly true of standard machines such as turning lathes, milling machines, laser cutting machines, press brakes and similar.

The costs of a machine tool comprise the following:

- Buying price of machine

- Energy costs

- Maintenance costs

- Working life of machine

Normally, machine tools in Germany are used for between 10 and 15 years. This working life is heavily dependent on the type of machine and on technological developments. For example, presses, large turning lathes or machining centres generally have a longer working life than laser cutting machines, spark erosion machines and machines with a high electronic content.

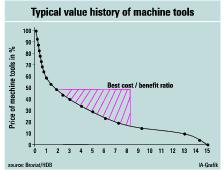

All machines have in general a similar rate of depreciation. The greatest depreciation always takes place in the first 2 years. Depending on the type of machine, this depreciation lies between 35% – 50% of the purchase price. Subsequently the depreciation takes place at a much lower rate, depending on the type of machine usually between 5% – 10% per year.

If, for example a machine has already had a working life of eight years, the depreciation is low but there are, on the other hand, increasing repair costs, maintenance and other costs. Moreover, in comparison to new machines, the wage costs on the old machines are higher because the productivity of a new machine is usually greater.

To sum up: Machine tools have the best cost/use ratio between the second and the 8th year. Thus the more expensive a new machine tool is, the more sense it makes to buy a relatively new second-hand machine.

Teilen:

{kind=link}